Custom Search

|

|

|

||

|

Unsatisfactory Food Items The subsistence supply system has quality assurance provisions designed to guarantee the receipt of wholesome, satisftactory food products. However, the system does experience breakdowns in specification standards is allowing some unsatisfactory products to filter into the supply pipeline. NONHAZARDOUS.- These food items do not meet expected or desired standards, but do not constitute a health hazard to personnel if consumed. A good example of this would be chicken wings in a box labeled breasts. HAZARDOUS.- These food items would possibly cause, or are suspected to have already caused, harm after being consumed. Determination of fitness for human consumption is the responsibility of the

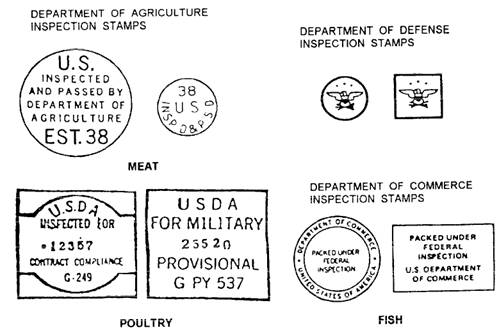

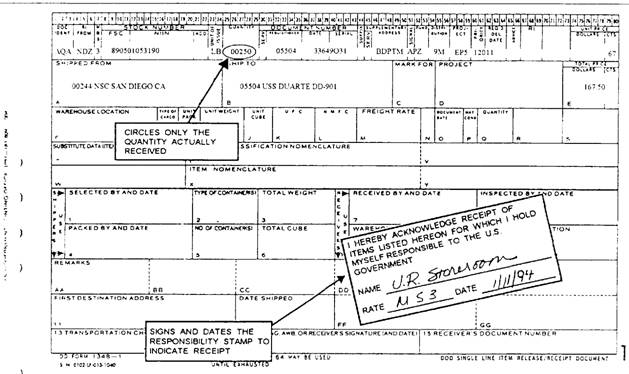

Figure2-l.-Meat, poultry, fish, and their by-products inspection stamps. medical officer. Examples of hazardous food item characteristics are widespread presence of swollen or leaking cans and products with either offensive or unusual odors and colors or any other evidence of deterioration. Refer to the NAVSUP P-486, volume I, for more information regarding the reporting and handling of nonhazardous and hazardous food items. It is always possible that several discrepancies can occur during shipment and receipt. All of these can be discovered during careful inspection and verification of receipts. The following actions will be taken when these discrepancies are found. SHORTAGES IN SHIPMENT.- A shortage occurs when the quantity received is less than the quantity shown on the receipt, regardless of the quantity on the original requisition. If a shortage exists, contact the issuer or shipper, either in person or by message, to try to resolve the discrepancy. Refer to NAVSUPINST 4440.179 for further guidance. Shortages due to transportation discrepancies will be reported according to NAVSUPINST 4610.33. Receiving activities will notify the supply/transportation officer of all transportation discrepancies upon their discovery. For all types of discrepancies, the receipt inspector and the bulk storeroom custodian will indicate on the receipt document the actual quantity physically received by drawing a single line through the invoice quantity and recording and circling the actual quantity. Both will then sign and date the receipt documents. (See figure 2-2 and 2-3.) Forward the documents to the FSO. When substantial shortages are found in shipments received from Navy supply activities (Navy supply centers [NSCs] or Navy supply depots [NSDs]) or combat logistics force ships (AFSs, AFs or AORs), you should immediately contact the issuer/shipper in person or by message to resolve the discrepancies. In the event shortages do exist after investigation, the full quantity and dollar value of the invoice will be posted to the Subsistence Ledger, NAVSUP Form 335; the Record of Receipts and Expenditures, NAVSUP Form 367; and the Requisition Log, NAVSUP Form 1336. The quantity and dollar value of the loss of $50 or more per line item will also be posted to the records according to the survey procedures found in the NAVSUP P-486, volume I. Losses of less than $50 per line item will be documented as a loss without survey. OVERAGES IN SHIPMENT.- An overage occurs when the quantity physically received exceeds the quantity stated on the receipt document regardless of the quantity on the original requisition or purchase order. When this occurs, immediate liaison is to be established with the issuer to resolve the discrepancies.

Figure 2-2.-Receipt by bulk storeroom custodian using DD Form 1348-1.

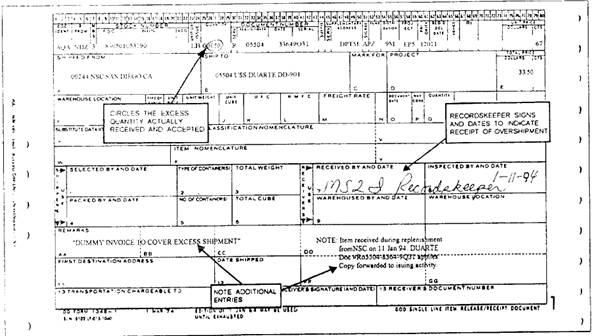

Figure 2-3.-Receipt by receipt inspector-shortage in shipment using DD Form 1348-1. Overages From a Navy Source.- When discrepancies from a Navy source are not resolved, the receipt inspector and bulk storeroom storekeeper should indicate the actual quantity physically received on the receipt document by drawing a single line through the invoiced quantity. Then both sign and date the receipt document. See figure 2-4 Forward this document to the FSO. A dummy receipt document should then be prepared to document the excess quantity received. This dummy receipt document can be a DOD Single Line Item Release/Receipt Document, DD Form 1348-1, or a Requisition and Invoice Shipping Document, DD Form 1149. See figures 2-5 and 2-6 for examples of these documents. In addition, mark on the document Dummy Invoice to Cover Excess Shipment to distinguish the dummy invoice from a normal receipt.

Figure 2-4.-Original invoice to cover excess shipment receipt by bulk storeroom storekeeper using DD Form 1348-1.

Figure 2-5.-Dummy involve to cover excess shipment using DD Form 1348-1.

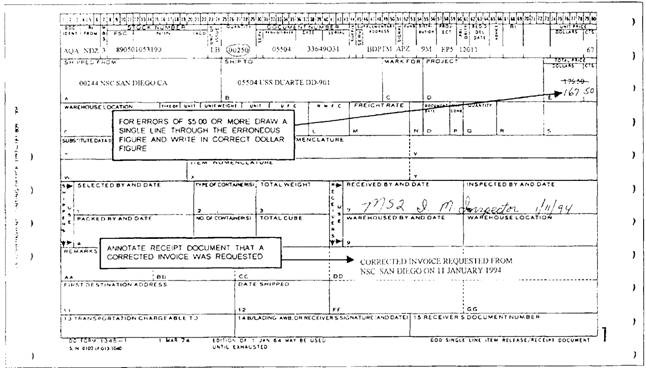

Figure 2-6.-Dummy invoice to cover excess shipment using DD Form 1149. It will also be used as the source document for posting the excess receipt. After the preparation of the dummy invoice document, the receipt inspector and bulk storeroom storekeeper will circle the excess quantity received, then both will sign and date the document. Forward the documents to the FSO. Overages From a Commercial Source.- When an overage occurs from a commercial vendor, the receipt inspector and bulk storeroom custodian will sign only for the requested quantities on the receipt documents and forward the documents to the FSO. Any excess quantities will be returned to the vendor. RECEIPTS WITHOUT INVOICES.- When food items are received without invoices or unpriced invoices, a dummy invoice will be prepared and the food items will be taken up at the last receipt price as shown on your current NAVSUP Form 335. When the price invoice is received, the receipt unit price rounded off to the nearest cent will be the unit price for the item. A cross-reference will be made on the priced invoice to its related dummy invoice and, if required, an additional line entry will be posted on the NAVSUP Form 367 for any difference. ERRONEOUS INVOICES.- An erroneous invoice is an invoice where the invoice quantity times the unit price does not equal the total dollar value. Erroneous Invoice From a Navy Source.- When an invoice is received containing an error of $5 or more, a corrected or credit invoice will be requested from the issuing activity. The error is lined through on the original receipt document (fig 2-7) , without erasing the erroneous figure and the correct amount will be inserted and posted to the NAVSUP Form 1336 and the NAVSUP Form 367. Upon receipt, the corrected or credit invoice will be filed with the retained records. Errors of less than $50 will be posted as is to the NAVSUP Form 1336 and the NAVSUP Form 367. The difference will be absorbed in the price adjustment at the end of the accounting period.

Figure 2-7.-DD Form 1348-1, an erroneous invoice. Erroneous Invoice From Commercial Sources.- When an invoice is received containing an error of any dollar value, a corrected invoice should be requested from the commercial vendor. The error will be lined through without erasing the erroneous figure and the correct amount will be inserted and posted to the NAVSUP Form 1336 and the NAVSUP Form 367. Upon receipt, the corrected invoice will be filed with retained returns. |

|

|

|

||